Mortgage Interest Rates

With all the attention focused on the likelihood of an upcoming Federal Reserve interest rate cut, and the effect it may have on mortgage interest rates, we are repeating the blog from last November which looks at the history of mortgage interest rates and the thought process that affects our monetary policy.

If the Fed reduces their interest rate, will mortgage rates be reduced as well? The Fed rate and mortgage rates are closely related, but they are not the same thing. So a Fed rate cut will not result in an immediate mortgage rate reduction, but over time mortgage rates should improve as well. Fixed rate mortgage interest rates are more directly influenced by changes in 10-year Treasury Bond yields.

A Look at Mortgage Interest Rates

John Andrews

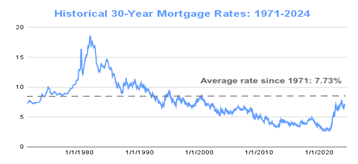

As a real estate licensee since 1973, I have witnessed mortgage interest rates as high as 18% and as low as 2%. This chart by Rocket Mortgage shows mortgage interest rates since 1971.

Who sets the rates and what factors affect their decisions? The first part of the question is easy to answer – the people who are lending the money make that decision. The second part of the question is more difficult to answer but supply and demand is a main underlying factor. Other factors are (in simple terms):

Interestingly enough, whether the rates are 18% or 2%, the real estate business continues by adjusting to the given situation. I can recall reverse amortization mortgages, split funding, wrap around mortgages, lease with purchase option, lease purchase and my favorite – owner financing.

Contact us at the Andrews Team to discuss current market and financing conditions.

Coastal Market Update March 2026

Foley Market Update March 2026

Foley Market Update February 2026

Coastal Market Update February 2026

Coastal Market Update January 2026

This is the market recap for December 2025.

This is the market recap for November 2025.

This is the market recap for the tenth month of 2025.

This is the market recap for the ninth month of 2025.

Discover your dream home on the Alabama Gulf Coast—partner with The Andrews Team for unmatched expertise and exceptional results. Start your journey today!